Forward this issue to your friends and urge them to subscribe.

Read all Life, Liberty, Property articles here, and full issues here and here.

GAO Confirms Enormous Entitlement Fraud

Video of the Week: DOJ Charges Southern Poverty Law Center — In the Tank Podcast #533

Who Is to Blame for Today’s Inflation?

GAO Confirms Enormous Entitlement Fraud

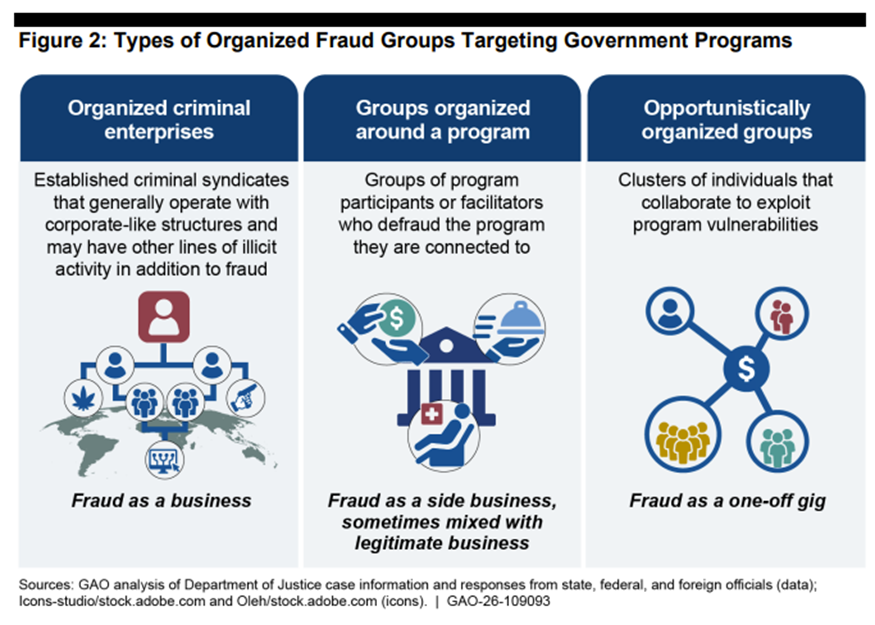

A new report from the Government Accountability Office (GAO) confirms that federal government programs paid out hundreds of billions of dollars of undeserved benefits to criminal organizations and other opportunists across the country in a five-year period. The agency’s forensic audits and investigative service director, Seto J. Bagdoyan, delivered the report as testimony to the House Committee on Oversight and Government Reform’s Subcommittee on Government Operations on Tax Day, April 15.

The report, “Combating Fraud: Challenges in Managing Fraud Risks in Federally Funded, State-Administered Programs,” covers programs such as Temporary Assistance for Needy Families, Medicaid, the Supplemental Nutrition Assistance Program, multiple housing programs, Unemployment Insurance, and many more:

In 2024, we estimated that the federal government loses between $233 billion and $521 billion annually to fraud, based on data for fiscal years 2018 through 2022. The range represents 3 percent to 7 percent of average federal obligations during that period. The width of the range is a reflection of both the uncertainty associated with estimating fraud and the diversity in the risk environments that were present in fiscal years 2018 through 2022. Given the time frame of the data, the estimate includes pandemic-related spending. The estimate also captures losses that occur at the state, local, tribal, or other government level if those losses included a federal investigative, administrative, or related action.

(Note: I removed footnote callouts from all quotes of the report, for ease of reading.)

As I noted in Life, Liberty, Property #131 (“The Fraud Is Worse Than You Ever Imagined”), the very structure of these programs invites fraud, robbing the taxpayers and diverting money from the 74 million Americans who receive entitlement payments. The GAO report confirms this:

There are many reasons and benefits to having federal programs administered through states. However, this approach exponentially increases the scale of government transactions across the states and U.S. territories. The programs can vary in size, but some, such as Medicaid, involve tens of millions of beneficiaries. When payment or eligibility decisions are made outside of federal agencies, fraud risk heightens.

For example, the Council of the Inspectors General on Integrity and Efficiency reported in January 2021 that grant programs—such as the Temporary Assistance for Needy Families (TANF) block grant that is funded by the U.S. Department of Health and Human Services and administered by states—faced an increased risk of fraud, waste, and mismanagement because of limited visibility and control over expenditures at the award recipient and subrecipient levels. Additionally in May 2020 and October 2021, the Mississippi State Auditor announced that multiple individuals affiliated with that state’s TANF program potentially misspent, converted to personal use, or wasted more than $77 million of TANF grant funds.

Decentralized program delivery—where federal funds are distributed to grantees, subrecipients, contractors, and subcontractors—also creates vulnerabilities to different types of fraud. For example, in May 2021, we found the decentralized environment makes the Community Development Block Grant Disaster Recovery (CDBG-DR) vulnerable to certain types of fraudulent schemes as money flows from the Department of Housing and Urban Development to several entities, including states, before reaching their intended beneficiaries. These schemes include contractors providing false certification of qualifications or eligibility, fraudulently billing after taking a deposit and receiving CDBG-DR funds, and conspiring to influence the procurement process to circumvent competitive bidding controls.

In short, state governments are promoting this enormous theft through negligence and deliberate disregard of their obligations to ensure the benefits are distributed according to federal law. The state governments treat eligibility verification as a very low priority, or none at all, regularly operating under the assumption that recipients are honestly stating their needs. The federal government and the states allow the fraud to occur and then go after a very small percentage of the thieves, if any, the report observes:

[P]rograms have too long relied on the costly and ineffective “pay-and-chase” model, which refers to the practice of attempting to recover funds after payments have been made. This approach was particularly evident during the COVID-19 pandemic for programs administered at the federal level, such as the U.S. Small Business Administration (SBA)’s programs to support small businesses and retain employees, and for programs at the state level to support individuals, such as the Department of Labor’s (DOL) UI programs.

We have found that federal and state agencies relied on self-attestation or self-certification for individuals and entities to verify their eligibility or identity to receive assistance from some COVID-19 relief programs, in an effort to disburse funds quickly to those in need. Even when program design decisions allow for self-certification, agencies are responsible for designing and implementing control activities to prevent fraud. Self-certification alone is not sufficient as a fraud control to mitigate misrepresentation.

Even states that want to confirm eligibility have difficulties because of the structure of the system and federal government requirements. The report states,

[A]s part of our 2025 work on organized fraud groups, we found that state officials specifically cited challenges related to data limitations and program delivery. For example, a state official told us that each program is restricted to sharing data within the program. There are also limits to interagency information sharing. For example, one state agency administering a federally funded program reported that it is restricted by state and federal laws from sharing information with other programs in the state, such as information on individuals and the state services they use. This restriction can limit the ability to connect fraudsters to potential fraud within and across state programs. Federal officials also told us that obtaining critical data, such as tax records to verify an applicant’s identity or program eligibility, is time and resource intensive while also safeguarding the data.

The report identifies three major types of organized fraud groups that steal from the taxpayers through these programs:

The “pay and chase” reliance on self-certification has allowed this type of crime to expand into a multibillion-dollar enterprise for fraudsters, the report notes:

Our prior work examining SBA’s Paycheck Protection Program and COVID-19 Economic Injury Disaster Loan program fraud schemes identified (1) ineligible, nonoperating businesses that applied for, and obtained, program funds; (2) legitimate business owners misrepresenting eligibility regarding their criminal record, federal debt, or principal place of residence, among others; and (3) falsification of tax or other documents to obtain more funds. In these instances, recipients falsely self-certified eligibility. As we reported, other fraud controls to mitigate these misrepresentations were either not in place or were not effective for those programs. Confirming eligibility of individuals receiving benefits, such as by confirming wage information or by verifying identity through data and other checks, are key controls to prevent fraud schemes that rely on mechanisms such as misrepresentation.

Although the report covers the Covid era in addition to the years around it, the observations apply to the structure of federal funded, state-administrated programs in general. “Self-certification alone is not sufficient as a fraud control to mitigate misrepresentation,” the report states.

Fraud has become a highly lucrative business for criminal enterprises under this approach, and it adds to the already enormous burden these programs place on taxpayers. States and the federal government must work together to end this theft of taxpayer dollars. Most importantly, the federal government must ensure that states exhaust all possibilities in rooting out fraud, given that the feds are the ones who create and maintain these programs. The report states,

Commitment to fraud risk management must start with leadership, setting the tone at the top that acknowledges fraud risks, commits attention and resources to manage them decisively, and communicates the value of fraud risk management. … The objective of fraud risk management is to ensure program integrity by continuously and strategically mitigating the likelihood and impact of fraud. This objective is meant to facilitate achievement of the program’s broader mission and strategic goals by helping to ensure that funds are spent effectively, services fulfill their intended purpose, and assets are safeguarded.

This vast theft of taxpayer money robs the nation’s taxpayers and the people for whom these programs are intended. The report states,

[E]very dollar or resource that is diverted to fraudsters hinders the federal government’s ability to achieve its goals. Direct financial losses from fraud place an increased burden on the government’s financial outlook. Additionally, nonfinancial impacts and losses erode public trust in government and hinder agencies’ efforts to execute their missions and program objectives effectively and efficiently.

That is undeniably true. The federal government borrows much of the money for these programs, placing the burden on expected future taxpayers and on current taxpayers through interest on the federal debt, and it takes money for these programs surreptitiously through price inflation. All of this is an unnecessary burden on current and future taxpayers.

More than half of all federal spending goes for entitlements. Federal entitlement spending in Fiscal Year 2025 was budgeted at $4.18 trillion, out of a $7.01 trillion overall budget. The 2026 budget allotted $531 billion in net interest payments on the federal debt.

This spending is unsustainable. The necessary federal borrowing pushes up interest rates and diverts investment from productive enterprises. These factors are pushing the nation toward an unstoppable debt spiral.

The only way to avert a cascading collapse of the federal government, the U.S. economy, and the nation’s political system is to reduce spending to the 2019 levels and then continue to cut from there. In such circumstances, any waste in the system is unjustifiable and in fact unconscionable. Congress and the president must act swiftly to eliminate fraud in federal and federal-state programs, and then undertake the even more daunting task of reducing spending across the board.

Unfortunately, there does not appear to be any appetite for such commonsense reforms. That appears to be the greatest fraud of all.

Get the latest best-seller from Heartland’s Justin Haskins!

America’s economy is teetering on the edge of disaster. Hidden beneath record stock market highs and reassuring headlines lies a fragile system riddled with debt, reckless speculation, and decades of political negligence. When the next big crash strikes—and it will—the fallout could be unlike anything we have ever experienced.

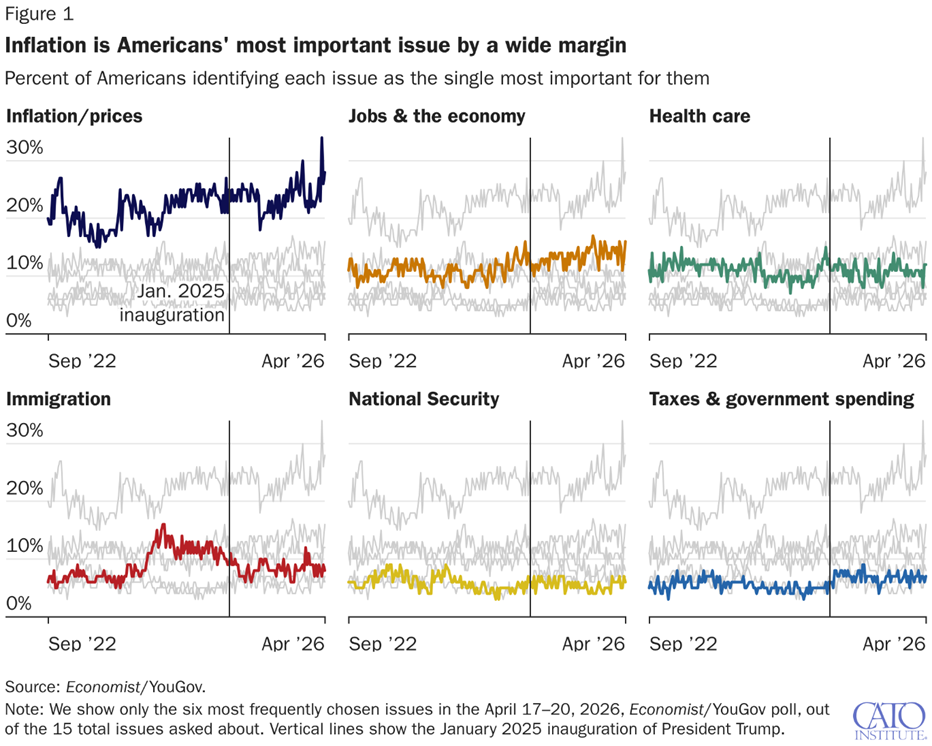

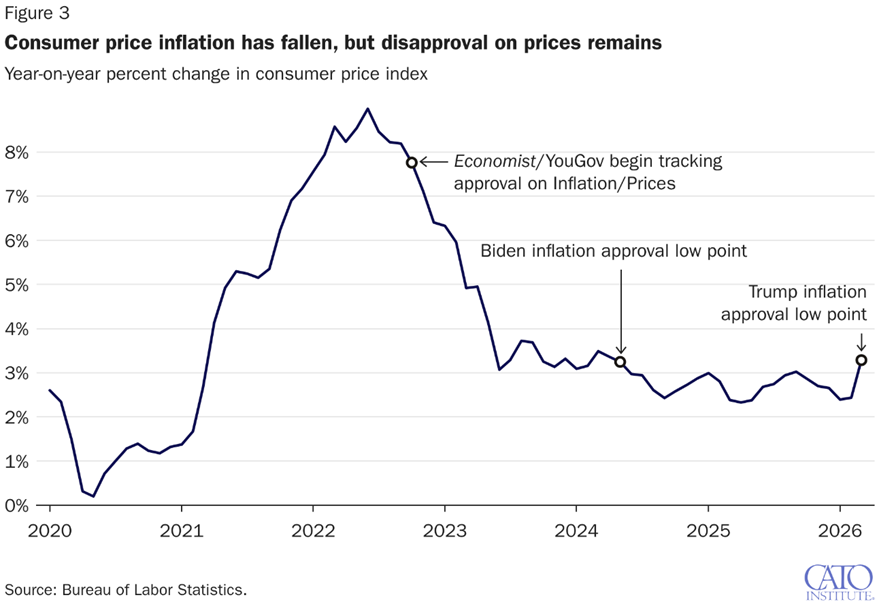

The affordability crisis that has received so much attention in the past 15 months is an outcome of the severe price inflation of 2022 and 2023. Economists Ryan Bourne and Nathan Miller, writing at their excellent blog, The War on Prices, note that Americans rank inflation as the most important issue today and blame the current president for the problem:

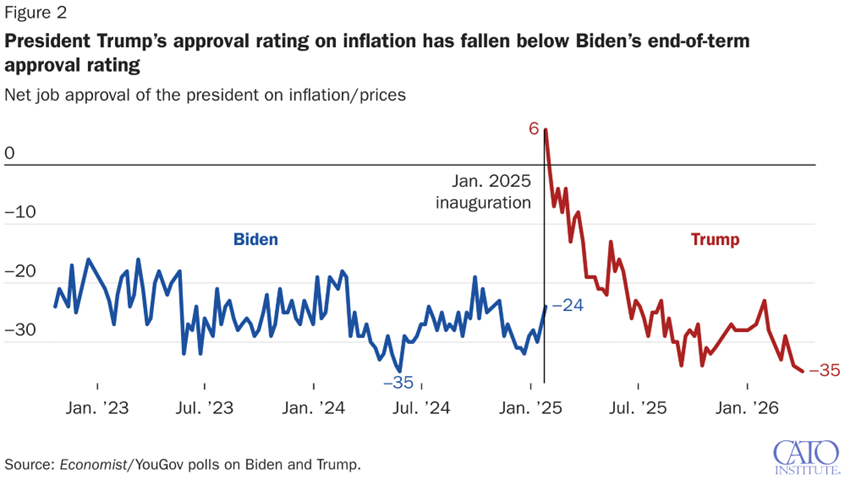

The recent high inflation is still claiming new political victims. Economist/YouGov polling shows 28 percent of Americans now name inflation or prices as their most important issue, almost double the share citing jobs and the economy (the second most pressing). The share of Americans picking inflation has consistently hovered between 20 and 30 percent recently and hit highs of 34 percent in early April. Donald Trump, as the incumbent president presiding over all this, finds his net approval on inflation now deeply underwater.

Bourne and Miller include a Cato Institute chart that shows inflation is a bigger concern than when it was much higher than today (9.2 percent inflation in June 2022 versus 3.3 percent in March, which was itself anomalously high, having been pushed up by a brutal onetime increase in oil prices caused by the Iran conflict), and that almost nobody cares much about taxes and government spending:

As I have been reporting over the past year-plus, the inflation surge of 2022-2023 is to blame for the public’s subsequent concerns about the shrinking dollar. Bourne and Miller agree with that assessment:

But this polling doesn’t look, primarily, like a backlash to the latest oil-price fears or the Iran conflict. The better reading is that Trump is suffering because voters are still angry about the earlier inflation surge and the fact that the price level never came back down.

I think that’s exactly what has happened. Bourne cites an article he wrote for The Washington Post, published last Tuesday, where he states that although Trump has pushed some inflationary policies (which have not done the expected economic harm, other than the Iran conflict), the Biden inflation is still plaguing the economy, and Trump is the victim of public disappointment over a problem he did not create:

The deeper explanation, though, is that voters remain furious at the rise in costs from the inflationary period of 2021 to 2025. Since Trump cannot reverse those high prices, their disillusionment has grown.

In their Substack post, Bourne and Miller show that Trump’s rating on inflation began to decline as soon as he took office, unrelated to anything he did and irrespective of subsequent variations in the inflation rate:

Trump’s political deterioration on inflation began well before the Iran conflict. His net approval on handling inflation/prices fell steadily from his inauguration, from +6 approve-disapprove to a low of -34 late last year. There wasn’t an obvious breakpoint after Liberation Day or other policy announcements. There is a small deterioration after early February (-28) that likely reflects the Iran conflict, but most of the damage had already been done.

Voters are angry because of where prices are now, even angrier than they were when inflation was at its recent peak in 2022, Bourne and Miller note:

Trump is now as unpopular on inflation as Biden was at his lowest. Trump’s roughly -35 net approval on inflation now matches Biden’s low from May 2024. But CPI inflation today is about 3.3 percent, nowhere near the 9 percent peak Biden oversaw in June 2022. When the Economist/YouGov began tracking inflation approval in late 2022, CPI was still near 8 percent, yet approval fell as inflation moderated, bottoming out once it became clear that disinflation had stalled above 3 percent and the price level wasn’t coming down. That strongly suggests voters react to the price level rather than contemporary inflation rate, and that fact has endured over Trump’s presidency to date.

The Biden-era inflation surge is the source of people’s current worries about prices, Bourne and Miller write:

What they are reacting to is the legacy of the 2021–2025 price surge. The most plausible explanation is that voters are still furious about the higher price level left behind by recent inflation, and they blame Trump for failing to reverse it. This is less about current monthly inflation prints or policies (although on the margin, tariffs, pressuring the Fed to lower interest rates, the Iran war, etc. don’t help) than about the fact that everyday essentials still cost far more than they used to in 2021.

Although he did not cause the inflation, Trump is to blame for having repeatedly claimed that he would bring prices back down to where they were before, a promise impossible to keep. Bourne discusses that in his Post article:

According to a poll from Echelon Insights, 80 percent of likely voters thought the president would reduce prices once back in office. But while egg prices fell and gas got cheaper until recently, presidents can’t influence overall price levels as directly as Trump’s campaign speeches suggested. Grocery costs, utility bills and mortgage rates continue to give American families profound sticker shock. The Echelon poll also found that 74 percent of likely voters won’t believe inflation is solved unless prices fall. Since they haven’t, and won’t, the president gets blamed.

The public appears to have been traumatized by the 2022-2023 inflation and is misreading the current inflation rate as a result. Bourne and Miller write,

The inflation shock therefore seems to have rewired how Americans think about “inflation.” After a long period of relative price stability, the 2021-2025 surge has apparently made the public far more sensitive to the price level itself. Many Americans now use “inflation” to mean “prices are still too high,” not “prices are still rising rapidly.” Real earnings growth last year didn’t appear to dissipate concerns about affordability either. If real wages keep rising and time passes, history suggests eventually voters surely won’t care about the legacy of 2021-2025 on the price level. But right now they are highly attuned to it given its recency, and want a politician to bring prices down.

Bringing prices back down to their previous levels would require a major deflation, which would involve a severe tightening of the money supply. That would almost certainly cause a recession, which no sensible politician wants. Another solution, and a better one, would be for Congress and the president to cut spending and federal borrowing, which would reduce the need for the Federal Reserve (Fed) to print money to cover ever-expanding government debt, known as monetizing the debt. The politicians do not want to do that, either.

Instead of doing the right thing, politicians are engaging in a theatrical “war on prices,” Bourne and Miller note:

Faced with anger about the effects of inflation on the price level, politicians of both parties are scrambling around proposing price controls, subsidies and various forms of regulation to try to reduce specific prices of life’s essentials.

In his Post article, Bourne makes the same recommendations I have been advocating: lower federal spending, cutting regulations, and limiting the Fed’s mission to monetary stability. Bourne writes,

If politicians were serious about dealing with the public’s discontent about prices, they would start by anchoring the Fed to a clear policy rule and stripping away its distracting regulatory functions. This would reduce the risk of the Fed hand-waving away inflation and tightening policy too slowly. Congress should also control the federal debt, which threatens to undermine the Fed’s independence and fuel future inflation as pressure builds on the central bank to help the federal government avoid spiraling interest costs.

Short of that, Trump could at least harness the deregulatory instincts of his first term. Government policies at every level inflate the costs felt by American consumers. Zoning and permitting rules strangle the housing supply, energy restrictions and tariffs raise utility bills, and agricultural mandates and tariffs increase food prices. Just as in the 1970s and ’80s, when deregulation of air travel and trucking lowered costs, liberating supply in these markets could reduce prices in ways that political theater about price gouging never will.

Trump has, in fact, been solid on deregulation, to the extent that the president can deregulate things under current law. Trump’s energy reforms attest to that. In addition to his criticisms of Trump’s tariffs, what Bourne appears to be calling for is major congressional action to deregulate multiple industries. That has not happened in almost a half-century, and this Congress is certainly unlikely to break that tradition.

With all good options off the table, somebody is going to take a beating this November for inflation, and that “somebody” is not going to be the ones who caused it.

The Heartland Institute 1933 North Meacham Road, Suite 559 Schaumburg, IL 60173 p: 312/377-4000 f: 312/277-4122 e: [email protected] Website: Heartland.org